Lifestyle

How Britain has changed financially during the Queen’s reign

In June, streets up and down the UK put up bunting as the nation marked the Queen’s 70th year on the throne. As the longest reigning British monarch, she has been a constant while many aspects of British life have changed.

70 years ago, just 14% of households owned a television, and there was only one channel to watch. Fast forward to today, and 95% of households have one or more televisions, from which viewers can usually choose from a myriad of channels and streaming services.

Another change has been the UK’s financial landscape, and the way Britons now deal with their money. For example, the days of visiting your bank manager to discuss your bank account or a loan have largely gone, as internet banking is today the norm.

Read on to take a trip down memory lane and discover five key changes to Britain’s financial landscape and the way we deal with our finances since the coronation in 1952.

1. The way we pay for goods has changed dramatically

The way we pay for the items we buy has changed significantly. Seven decades ago, people generally carried cash to pay for items and, in 1952, the UK still used the “shilling” as currency.

This was lost in 1971 when Britain “decimalised”, and pence and pounds became the main legal tender.

In 2022, carrying cash is much less common as people now pay for goods using payment apps or debit cards. Today, 98% of Britons use the cards, which were first introduced in 1987.

When the Queen took to the throne in 1952 credit cards were unheard of. That changed when Barclays issued the UK’s first credit card in 1966, and today, more than two-thirds (69%) of adults use a credit card to buy goods.

In 1997 the Nationwide Building Society introduced the first ever internet banking service, and by 2020, nearly three-quarters of adults (72%) banked online.

2. There is more choice around retirement

In 1952, men were entitled to the State Pension at the age of 65, and women at the age of 60. At the time, the pension was £1.62 a week, or £84.50 a year.

Today, the State Pension Age is 66 for everyone, and in 2022/23 pays £185.15 a week, or £9,627.80 a year, if you’re entitled to the full amount.

Seven decades ago, people generally left work when they reached State Pension Age, although that’s largely no longer the case. According to abrdn, in 2022, 66% of people plan to continue working past the State Pension Age, whether for financial reasons or to keep themselves occupied.

A key change to the way you’re allowed to finance your retirement happened in 2015, with Pension Freedoms legislation. It allows retirees to flexibly access their money purchase pension schemes from the age of 55, meaning retirees can either withdraw cash, purchase annuities, or both.

3. More Britons now invest their money

Seventy years ago, investing was a lot less common as it was seen as a “rich man’s game”. Today, however, many people have Stocks and Shares ISAs or pensions that are exposed to the stock market.

According to Schroders, between 1952 and 30 May 2022, UK equities returned an average of 11.7% a year. That’s significantly more than the 6% you would have earned if your money was invested in cash savings (proxied by short-term Treasury bills).

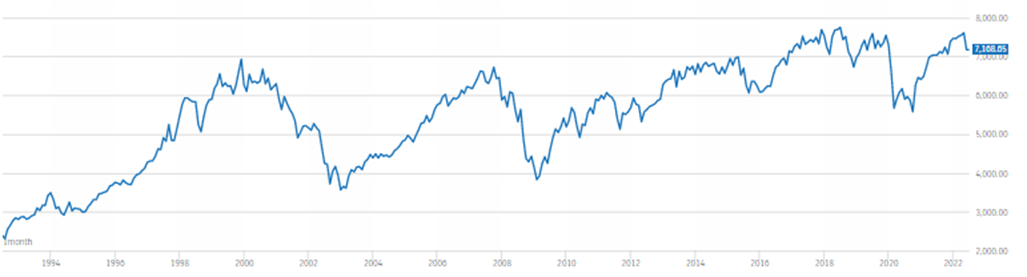

That said, stocks and shares have seen some significant downturns during the period. This is highlighted in the following illustration, which shows the performance of the FTSE 100 between July 1992 and July 2022.

The index follows the performance of the top 100 companies registered on the London Stock Exchange.

Source: London Stock Exchange

As you can see from the right-hand axis, while there have been major downturns along the way, the index increased significantly in value during these three decades. Please remember, past performance is no guarantee of future performance.

4. House prices have risen faster than average earnings

House prices were around six-times average earnings in 1952, meaning the average house price was around £1,800 and the average annual income was around £300.

According to Schroders, in 2022 the average wage is £32,000, yet the average house price is nine-times that amount, at £278,000.

So, it’s no surprise that it’s harder for millennial first-time buyers to get on the property ladder nowadays than it was for previous generations.

5. The way we shop has changed dramatically

In 1952, less than 1 in 10 people owned a fridge compared with 98% today. As such, many people used tinned food and grew their own vegetables to feed themselves, and typically bought produce from the butchers, bakers, and grocers more often.

Today, it’s more common for consumers to buy frozen or convenience foods, and to visit a supermarket once a week.

How Britons spend their money has been tracked by the Office for National Statistics, as it uses a virtual shopping basket to calculate the nation’s rate of inflation. The basket typically comprises of 700 items that change over time in line with the nation’s shopping habits.

Items that have been added and removed over the last 70 years include: condensed milk, corned beef, doughnuts, the “party seven” beer can, men’s suits, and corsets. Today the basket includes meat-free sausages, sports bras and anti-bacterial wipes.

Get in touch

We hope you found this blog enjoyable. If you would like to discuss your finances and wealth, please give us a call on 0800 434 6337. We’d be happy to help.

Please note

This article is for information only. Please do not act based on anything you might read in this article. All contents are based on our understanding of HMRC legislation, which is subject to change.

The value of your investments (and any income from them) can go down as well as up and you may not get back the full amount you invested. Past performance is not a reliable indicator of future performance. Investments should be considered over the longer term and should fit in with your overall attitude to risk and financial circumstances.

A pension is a long-term investment. The fund value may fluctuate and can go down, which would have an impact on the level of pension benefits available. Your pension income could also be affected by the interest rates at the time you take your benefits.

Have My Cake And Eat It

A change in lifestyle