Financial Planning

Why fixed-rate savings could still reduce your money in real terms

According to This is Money, those looking for better returns are putting their cash into fixed-rate savings. It reveals that almost half of savers are looking at fixed-rate deals to get higher rates of interest and better growth on their money.

While on the face of it, it may seem like shrewd financial planning, in reality it could still mean your money drops in real-term value because of rising inflation. And it may get worse, as the Bank of England (BoE) predicts inflation could continue to rise throughout 2022.

Read on to learn more about inflation and what you might do to better protect your wealth from its effect. Before you do, we need to consider why nearly half of all savers are opting for these deals.

Interest offered by fixed-rate accounts has risen in 2021

This is Money reveals that the rise of smaller, challenger banks in Britain has resulted in high street banks increasing their fixed-rate interest rates in a bid to fight back.

The article points to Al Rayan Bank, which in November 2021 offered the best one-year fixed rate at 1.45%. This was 0.78% higher than the best one-year easy access rate, which was being offered by Shawbrook Bank.

The article also showed that Al Rayan Bank was offering 1.76% for a two-year fixed rate and 1.81% for a three-year account.

This all sounds like good news, especially when you consider the Times reports that interest rates are expected to reach 1% by the end of 2022 – something that may push fixed-rate deals even higher.

In reality though, it may not be quite as good as you may hope. To explain why, we now need to look at inflation.

Inflation could still devalue your cash in real terms

As inflation is the rising cost of living, it affects almost every area of your finances, from your weekly shop to your energy bills.

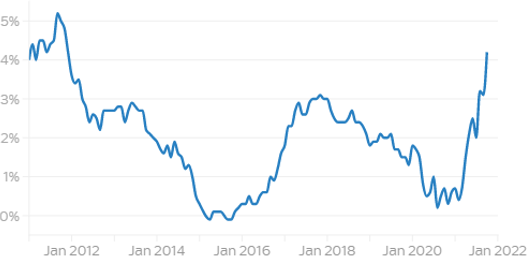

As the graph below illustrates, inflation rose sharply during 2021 as the UK got back on its feet economically after lockdown. According to the Office for National Statistics, it reached 4.2% in October 2021, which as you can see, is the highest level for almost 10 years.

Source: Sky News

Worse still, the BoE has also reported that it believes inflation could rise to 5% by the end of 2022.

To put this into context, consider the following: if you use an inflation calculator, you’ll see that in December 2021 you would need £137 to have the same spending power as £100 in 2010.

In other words, your cash needed to grow by 37% during the period to counter inflation, which stood at an average rate of 3% during the period.

All this means that, even with the fixed-rate deals being offered, the value of your money could still drop in real terms because they’re significantly below the rate of inflation. What’s more, this could still be the case if interest rates rise in 2022.

Investing could help inflation-proof your money

It’s not all bad news though. One way to potentially inflation-proof your cash could be to invest it.

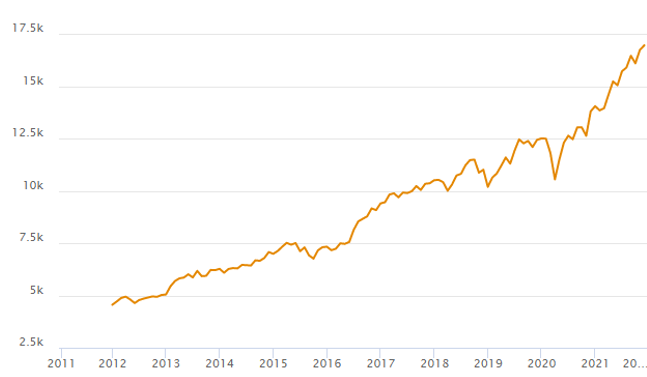

Investing could provide greater growth potential, as the following graph reveals. It shows the performance of the MSCI World index since December 2011, which tracks the performance of a basket of companies from 23 developed nations across the world.

As you can see from the values on the left-hand axis, despite downturns along the way, its value has increased significantly during the last 10 years. It shows that investing your money could provide better long-term returns than fixed-rate savings, and keep pace with rises in the cost of living.

Please remember, past performance is no guarantee of future performance, and you should never enter into investing lightly. Always take professional financial advice and treat it as a long-term venture.

A tax-efficient Stocks and Shares ISA might help

With this in mind, you may want to consider switching from a fixed-rate savings account to investing to potentially inflation-proof your money. One way you might do this is to use a Stocks and Shares ISA.

Any growth your investments make will normally not be liable to Capital Gains Tax, and any withdrawals will usually be free of Income Tax.

As moving your cash into a Stocks and Shares ISA increases the amount of risk your money is exposed to, always speak to a financial planner before going ahead. They can confirm the risks involved, the growth potential of your investments, and any charges you may incur.

Furthermore, they can confirm whether investing is right for you.

Remember, in the 2021/22 tax year you can put up to £20,000 into an ISA. If you don’t use all of your ISA allowance, you lose the unused amount at the end of the tax year.

Get in touch

If you would like to discuss a Stocks and Shares ISA, or other ways you might be able to inflation-proof your money, please contact us by calling 0800 434 6337. We will be happy to help.

Please note:

This article is for information only. Please do not act based on anything you might read in this article. All contents are based on our understanding of HMRC legislation, which is subject to change.

The value of your investments (and any income from them) can go down as well as up and you may not get back the full amount you invested. Past performance is not a reliable indicator of future performance. Investments should be considered over the longer term and should fit in with your overall attitude to risk and financial circumstances.

Have My Cake And Eat It

A change in lifestyle